Most financial professionals preach the positives of diversification. They promote it as much for risk mitigation as they do for obtaining superior returns. During prior times with more separate economies, more regional trade, markets that were less connected and less accessible to all, it was most-likely true. This has changed as trade, money movements and economies have globalized.

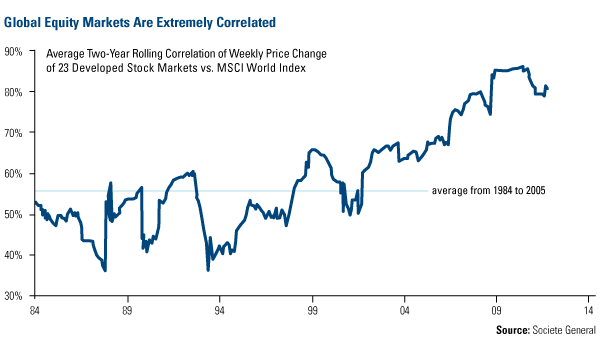

In addition, business cycles have become less dependent on long-cycle industrial activity (an interesting topic all on its own), and we start to see economic downturns impacting all markets at the same time. The result is diversification has little benefit in times of broad market panic.

Asset correlation is a phrase used in the financial world. Simply stated, it is the level of common movement between various asset prices. Correlation does not take into account the magnitude of movement. It only measures historical relationships. Although correlation does have some explanatory powers, it must be viewed skeptically as it represents an average. Meaning, it is approximately right over a long term, but will be precisely wrong at any specific time. We only bring this to your attention as it is vital to understand the limitations of this measurement. Although correlation can assist in setting up a diversified portfolio over the long period, it has little power to protect assets during times of panic. Why? Let us attempt to answer below.

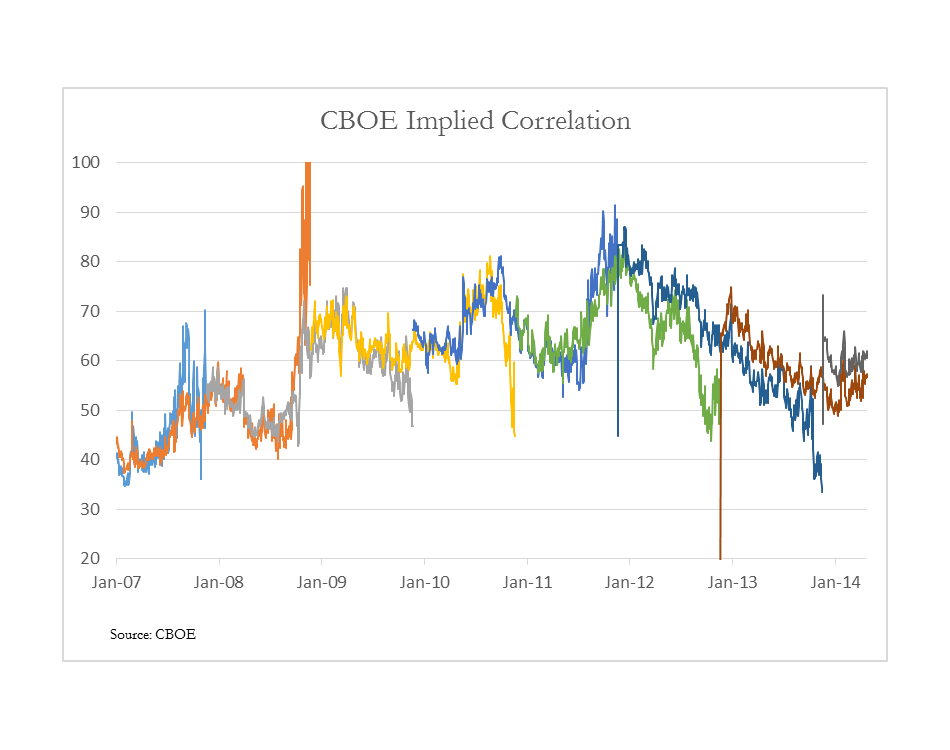

Although people will calculate the interaction between various financial assets (correlation), they will fall victim to the number when they believe it is static. It is not. Correlations change through time (see chart above) and when the proverbial “$?hit hits the fan”, correlations increase dramatically and all financial assets are moving in sync (see chart below). Correlation-based portfolios offer little protection in these situations.

How (Au)our Competitors Solve the Problem

We have seen various methods that attempt to protect portfolios in times of increasing asset correlations. One method, chosen by many, is simply to do nothing. This method relies on hand holding, glossy marketing material, slick talking points, and concert tickets as a distraction to alleviate the near-term pain clients will feel. Well dressed financial sales people will describe how over the long term clients will rebound and how client portfolios were well diversified, but the current economic events where ‘abnormal’. They espouse how few can “time the market” so therefore they do not try. They ultimately offer little value to their clients and offer distractions such as meaningless (yet effective) stories on how a client’s Berkshire Hathaway holding provides access to Warren Buffet’s investment prowess.

Investment firms that attempt to protect assets from falling during times of panic use, what we believe to be, very rudimentary techniques. They either sell assets after they have fallen (stop loss triggers) or, if they are quantitatively inclined, monitor the price volatility of various stock prices and sell when the volatility reaches a critical value. From our vantage point, these are analogous to “applying leeches to a wound” (Bloodletting went out of style a long time ago.) We believe it is time to give up crude “solutions” to asset protection.

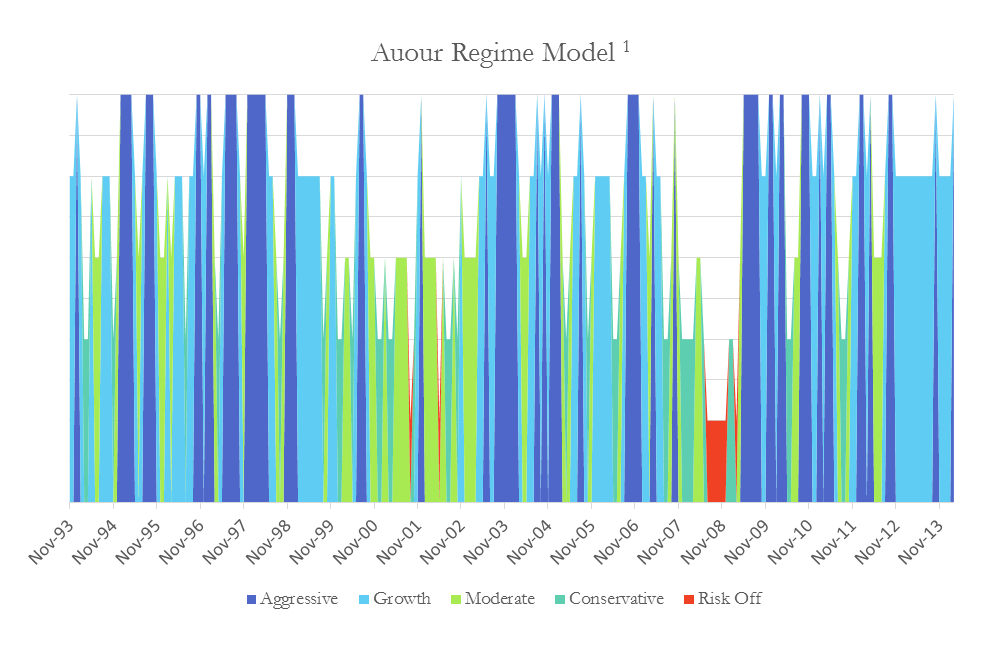

Auour Solution

We are advancing the idea of downside protection through the use of the Auour Regime Model (ARM) tool. This measure is the result of multiple fundamental factors that, based upon decades of investing experience, characterize the economic and investment environment. Rather than having the investment environment be a “rule of thumb” or a “gut feeling”, it has been defined by logic, honed with hard empirical evidence, and properly back tested to confirm its value.

As this measurement is proprietary, we will not discuss in any level of detail the factors that we evaluate. We will, however, say that it consists of observing movements of many asset classes from around the world, the ways they tend to act against each other, the liquidity and changing complexion of corporate financing, among others. These factors help us to objectively, and with some level of accuracy, gauge the spectrum of fear and greed that exists within the various financial markets of the world.

We will stop there. We could continue discussing this topic but there is a fair chance we have already put you to sleep. If any of you would like to understand our motives and methods in greater detail, we stand ready to explain to your heart’s content. Suffice it to say, we are excited (dare we say ebullient) in the progress we have made in this field of work.