We are strong believers in Peter Lynch’s quote, “Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections than has been lost in corrections themselves.” Because fearmongering market pundits profess that a correction is always near, we, therefore, continue to rely on Lynch’s statement.

There is no doubt that headlines these days are bad. North Korea becoming more emboldened in its desire to wreak havoc on the world as they defend their reign. The US government breaking new records for partisanship. Civility becoming second to rage in our own communities as extreme elements take to the streets. None of this feels good, especially to an investor base that, still remembering the damage done in 2008, witnesses new highs in global markets. Investors are on the edge of their seats, wondering, “Should I get out now?”

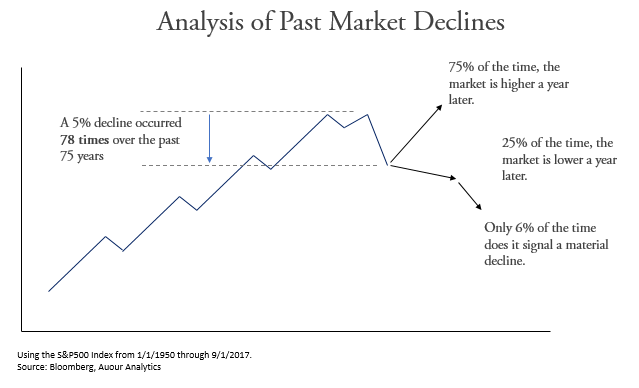

Downturns are painful, and while the fear that a few down days signal a larger decline is justified, they may not warrant a change in positioning. We went back over the last 67 years and reviewed the times the US equity market (using the S&P 500 index) suffered at least a 5% decline from its peak. We counted 78 times over that time span, about once every 10 months, where such declines occurred. Market commentators are discussing how we are due for a pullback given the market’s strength so far this year. Unsurprisingly, the last time the market dropped by 5% was November of last year — about 10 months ago.

So, history and averages predict a downturn sooner rather than later. Should we do anything to address it? Our answer is not yet. There have always been reasons to try to avoid mild drops throughout the year, but attempting to avoid a dreaded downturn in 2017 would have meant missing the approximately 15% upward movement experienced year-to-date. The missed return would have done more damage than the expected — but not-yet-experienced — downturn.

Prognosticating, “We are due for a correction,” is easy, but being right about such small movements is tough. With normal daily movements approximating 1% up or down, the odds are against you. Our review of the 78 times that markets experienced a 5% or larger decline shows that 75% of the time, the markets have returned to their pre-decline heights six and 12 months later, suggesting a shallow and short-lived correction. Only 6% of the time does a 5% correction lead to an enduring and material downturn in markets. The moral of the story is that reacting to what are typically normal market movements to protect wealth can diminish the power markets can provide to grow wealth.

We are not arguing for static positioning throughout the entire investment cycle. The costs of large and enduring downturns are real and should be minimized as much as possible. At Auour, we believe long-term downturns can be detected and losses minimized. It comes down to understanding when a normal downward movement has a high probability of being followed by a large loss.

We understand the importance of protecting capital. We are firm believers that long and deep downturns can make the most financially secure investor do the wrong thing at the wrong time when they fear an even longer and deeper bear market. We also understand the lost opportunity from not being invested in the equity markets. When markets have historically risen about 80% of the time, to refer back to Peter Lynch’s quote above, attempting to second-guess the short term can become counterproductive since the lost opportunity can be as costly as an anticipated correction.