“A person saving for retirement who chooses low-cost investments could have a standard of living throughout retirement more than 20% higher than that of a comparable investor in high-cost investments.”

– William Sharpe

Mutual funds that rely on stock-based investing where once a great idea. However, this investment vehicle’s time has come and gone. Their structure allowed the small investor to invest in a diverse portfolio of companies that was overseen by dedicated professionals. With time, however, things changed and markets evolved. Though mutual funds continue to be used by the public, they no longer offer the most effective way to invest an individual’s savings. The advances made in investment products and technology highlights the unnecessary costs associated with mutual funds and, generally, with stock-based investing techniques.

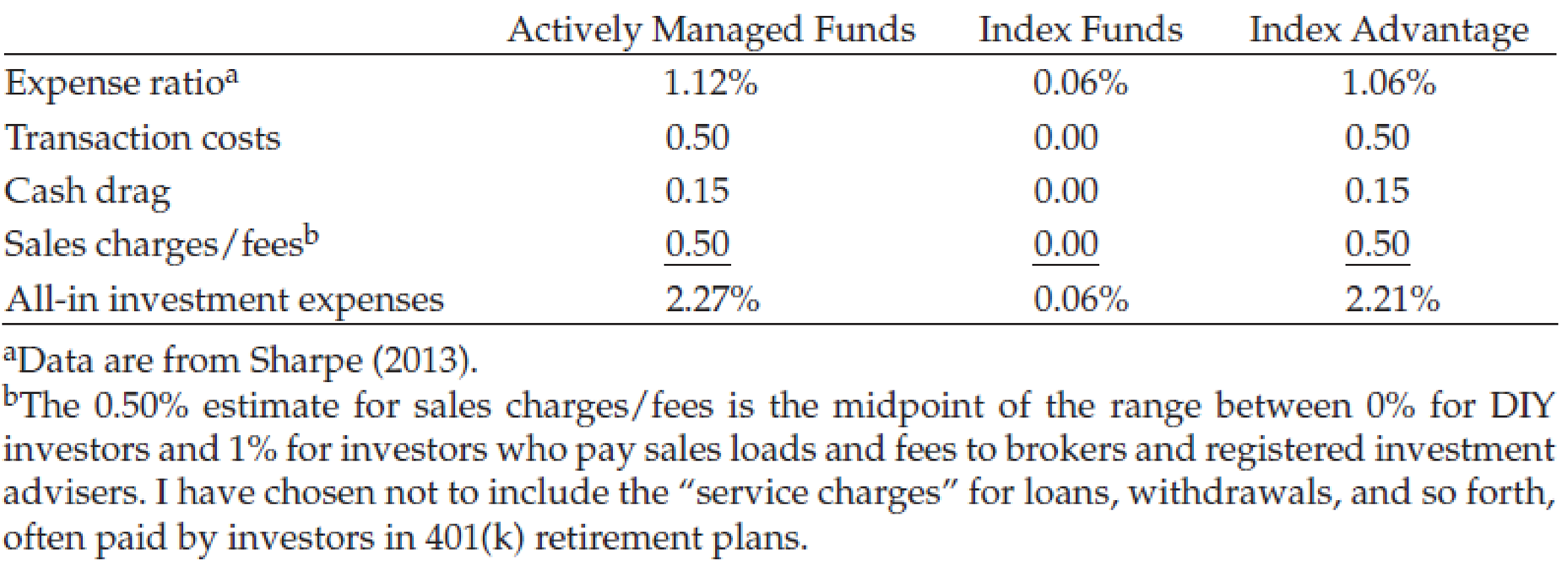

We have frequently highlighted that an individual has less than a 25% chance of finding a stock-based manager capable of consistently beating his benchmark. We haven’t yet spoken as to why this may be the case. Remember, stock managers are relatively bright individuals that nonetheless cannot beat their benchmarks. In the following text, we highlight research depicting the costs of running a mutual fund. We also show why the active stock-based manager starts at an upfront disadvantage, making attractive performance an even more unlikely outcome.

John Bogel, founder of Vanguard, wrote a paper for the Financial Analyst Journal in 2014 (Volume 70 Number 1) that does a wonderful job demonstrating the many hidden costs in mutual funds. These hidden costs result in the individual investor losing 50% of his investment profits. In short, if you own a mutual fund, there is an overwhelmingly large chance you are losing future purchasing power and risking the productivity of your hard earned savings. In order to clarify this concept with actual return numbers, a 7% market return will generally result in less than a 4% return to the individual investor. Additionally, these poor results are only available if you hold on through good and bad times. However, most investors do not do this, resulting in even lower returns.