Within the investment industry, there is an ongoing debate on passive versus active investing. Vanguard has been one of the more vocal participants at evaluating active managers and the consequences of stock-based investment strategies. Our own research into the matter confirms Vanguard’s hypothesis. Most managers that claim themselves to be active are not consistently adding value on top of the market’s natural return. Each year, we hear that this will be the year that active management wins, yet that seldom comes true.

This begs the question as to why?

A majority of the investment community attempts to add value by selecting individual stocks. They overweight one company or theme over others. Investment managers have been spending their time looking for inefficiencies within the valuation of individual companies in order to capture some extra return above the market’s. However, much like any free market, the more individuals focused on finding inefficiencies, the fewer inefficiencies there are to exploit. It therefore comes as no surprise that the large research staffs and immense research budgets of the largest mutual fund complexes are unable to outperform a passive collection of stocks. Their size and past success has resulted in an efficient market.

Does that leave us with only one solution, a static allocation of passive market weighted investments? No. Inefficiencies will always exist. The plan should be to seek out inefficiencies and exploit them. With nearly everyone “fishing the same pond” for individual company opportunities, maybe investors should find fishermen that have elected to change ponds and fish where ample opportunities exist.

Research consistently shows that the two largest components to one’s long term investment return are market participation and asset allocation. However, few of the large firms focus on those factors. Instead they focus almost all of their attention on finding the next Google, Proctor & Gamble, or Home Depot. This issue was highlighted in an October 20th, 2015 CNBC panel of leaders from three prominent mutual fund families. They all promoted active management focusing on stock selection. They all made claim that this is the year of the stock picker. When asked by the host if they ever make asset allocation calls or market participation calls, the CEO of one said they leave that decision to the client. The large investment firms readily admit to leaving the two most important investment decisions to the client.

As a result, it should not be a question as to why the mutual fund industry continues to see asset losses. Their leadership is void of comprehending the real need of the individual. Studies show that individual clients lose over 2% a year in annual return because they get scared out of the market at the worse time and reinvest at higher prices. Over 25% of the hoped-for return in the equity market is lost to mistiming. And yet, the investment industry has not structured itself to address this issue. That is until recently.

The financial crisis of 2008 acted as a wakeup call to investors and to some forward thinking asset managers. The historical method of a static allocation of diversified assets throughout the business cycle was found to be flawed. Diversification, the idea that a broad mix of asset classes, would save you from material losses during market downturns was proven wrong as almost all asset classes went negative. Diversification failed at the time it was wanted the most, creating a confidence crisis.

Being Active with Passive Vehicles

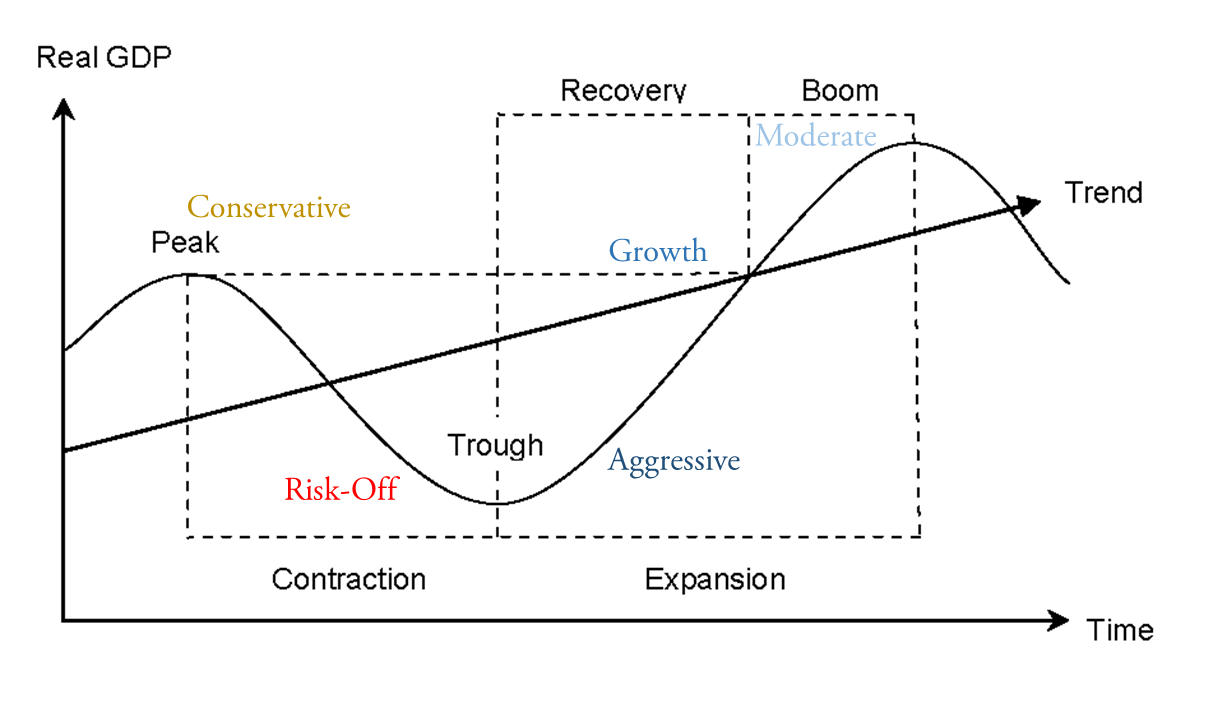

With the experiences of 2008 fresh in the minds of many, the idea that modern portfolio theory (MPT) is the solution to all investment problems was put into question. Research suggests that many of the inputs required for the application of MPT change throughout the economic cycle, leading to inefficiencies in portfolio positioning amongst the various stages of the cycle. With this new realization still not embraced by the larger investment firms, it has been the responsibility of new firms, such as ourselves, to pioneer this new insight of managing to the economic cycle. Using the knowledge that portfolio positioning should reflect the different phases of economic growth, we spend our time determining those phases and the asset allocations that improves our clients’ chances of succeeding throughout the cycle.

The implementation of this process, adjusting asset allocations based on economic cycle phases, elevates the focus to the area where inefficiencies are greatest: market participation and asset allocation. Firms advancing this process do not waste their time on the unproductive goal of determining which companies will outperform. Instead, the exposure to the desired asset class or style is obtained through lower-cost, passively-based investment funds.

In this new era, the debate of active versus passive goes away. The new firms that are gaining recognition are active participants. Like us, they choose to focus on the elements that have shown to be inefficient and accretive to client returns.