Historically, many countries have centralized their economies in an effort to improve productivity, raise living standards, and increase economic growth. In reality, the opposite has often occurred, resulting in stagnant economies and falling standards of living. Conversely, history demonstrates that creating increasingly open and fair markets activates economic potential that lay dormant under more authoritarian regimes.

This concept is particularly relevant currently, as we witness harm to the majority as a result of the hubris of the minority. Nowhere is this more evident than in the actions of central bankers across the world, US central bankers excluded at this point in time. Reminiscent of the old engineering adage, “If a hammer didn’t fix the problem, get a bigger hammer,” central bankers in developed international countries have continued to push rates lower in a failed attempt to engineer growth. Why does this strategy persist if it has seen little success and will likely continue to fail? We have no idea. Please call if you do!

Since their founding, modern central banks have tried to mitigate inflationary episodes by slowing economic activity through higher interest rates to offer a safer investment option. In the past, when people have been able to redirect excess savings into government debt, they have had less of a tendency to overinvest and over-consume. In times of lackluster growth — or recessions — with low inflation, central banks instead lowered interest rates, making positions in government bonds less attractive versus private sector investment and consumption. This inevitably led to increasing private sector investment and employment, enabling individuals to consume more.

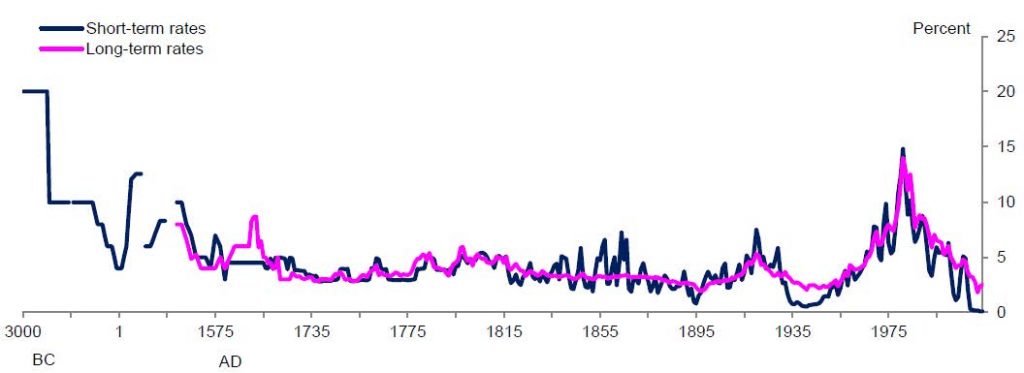

Raising and lowering interest rates worked well for many decades, but lowered interest rates’ ability to promote growth has vanished in many countries. But instead of rethinking the strategy, central bankers in Europe and Japan have instead begun to rely on a bigger hammer: negative interest rates, also known as the Negative Interest Rate Policy (NIRP). As of this month, the world sits on an estimated $10 Trillion of sovereign debt trading at negative interest rates. Just this week, the German 10-year Bund fell into negative territory. Currently, we are experiencing the lowest rates in recorded history.

Source: Andrew Haldane, Chief Economist of Bank of England, “Stuck”, Open University Milton Keynes. June 2015.

The hope has been that negative rates would push investment assets into higher yielding investment activities, with a side benefit of a softening currency to encourage exports. Unfortunately, the opposite has occurred as investors search for security and stability. Individuals in the private sector understand that money has a cost; though central bankers would like to convince them otherwise, investors recognize that economic system is unstable and are striving to preserve the wealth they have accumulated.

This is most obvious when examining the velocity of money. Economic activity is the product of money in the system and the number of times it trades hands over a certain period of time. The number of times money trades hands is referred to as velocity. The adjacent graph shows that the dollar’s velocity has been dropping to levels not seen in over 60 years. European and Japanese velocity measures are also hitting new lows.

This is most obvious when examining the velocity of money. Economic activity is the product of money in the system and the number of times it trades hands over a certain period of time. The number of times money trades hands is referred to as velocity. The adjacent graph shows that the dollar’s velocity has been dropping to levels not seen in over 60 years. European and Japanese velocity measures are also hitting new lows.

This is also supported by anecdotal evidence from Switzerland and Japan, where reports suggest that people are starting to pull money out of the banking system and store it in homes as safe sales have increased, causing some models to sell out (source). These acts are not what central bankers wanted or expected, and it is unclear whether or not they will be able to continue with their policies of negative interest rates.

Like any systems thrown into unstable states, these economies will inevitably move to more stable equilibria. What an equilibrium will look like, when it will arrive, how it will manifest, and what will catalyze its occurrence all remain very unclear, but one item that may instigate a move is US wage growth.

We are big believers in the concept that to have meaningful and persistent inflation, wage growth must be present. We have seen episodes where some items experienced inflation, but unless people begin to make more money, they will need to experience deflation in another part of their lives in order to maintain their standard of living.

We are big believers in the concept that to have meaningful and persistent inflation, wage growth must be present. We have seen episodes where some items experienced inflation, but unless people begin to make more money, they will need to experience deflation in another part of their lives in order to maintain their standard of living.

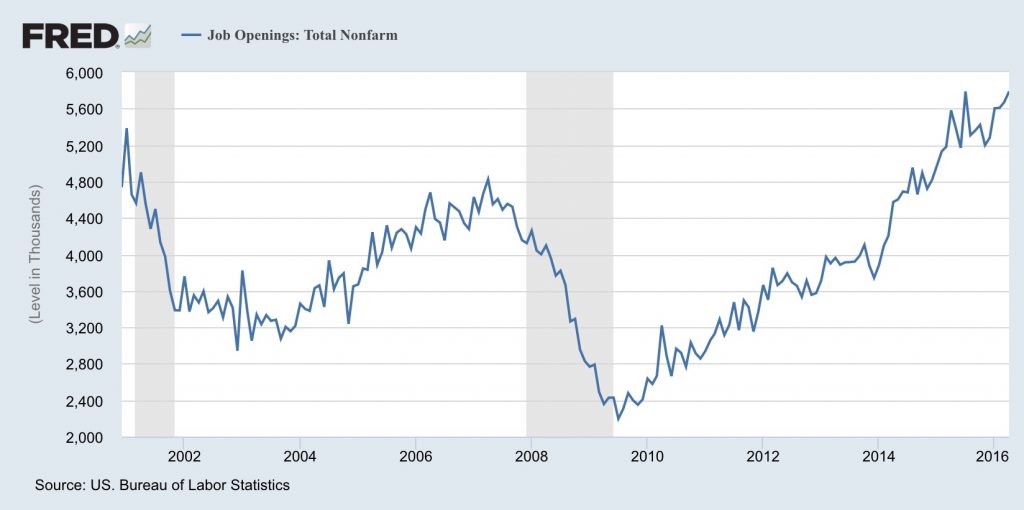

In aggregate, wages for the US population have been slowly recovering from the Great Recession. Although not yet back to the rates of the early 2000’s, wages have been steadily improving, and indications show that this trend will continue. One such indication is the number of job openings, tracked by the US Bureau of Labor. Over the last six months, the number of job openings is the largest seen.

The large number of job openings may also explain the recent surveys by the National Association of Colleges and Employers (NACE) that show starting salaries of graduates expanding at a 5% annualized rate for the past few years, suggesting a need to pay up to fill needed jobs.

To state the obvious, we are all traveling down a new path, bound to encounter many unknowns. The actions of central planners have had unexpected outcomes, resulting in unintended consequences that must be addressed. It is unsettling to recognize that, while global economies need to find a more stable equilibrium, no one has a clear idea of how to proceed toward that equilibrium. The continued strength exhibited by the US and the fact that millennials are now of an age to contribute meaningfully to society give us hope for the future of the economy. However, the economy is still subject to the manipulation of the anointed few, and we therefore remain guarded in our investment posturing.