October was quite a month for world markets, with many hoping November would be different. Though investors left the trough quickly for the second time this year, October’s losses felt different than February’s. February’s seemed merely ‘technical.’ October’s seemed more fundamental. The immediate context for February’s market losses were 13 months of positive returns, an optimism that the world economy was in a synchronized growth profile, and the reassuring sense that the impact of the new U.S. tax laws were still ahead of us.

The October selloff was different: World economies outside the U.S. are experiencing a material slowdown. China is proving that not all are wearing swimsuits as the tide goes out. (Refer to our 3Q commentary.) U.S. investors fear the positive effects of the tax laws are behind us. And with unemployment low, deficits rising, and inflation picking up, many are concerned that the best is now behind us.

We share some of those concerns. However, we started acting on them in the first quarter, and we see October’s movements as confirmation of the rationale behind the defensive position we took earlier in the year. On down days, it’s natural to wish you were more protected. Just as on up days, it’s natural to be happy you weren’t. Hyper-attention to short-term market movements—and the emotional baggage that come with them—is what our models aim to mitigate.

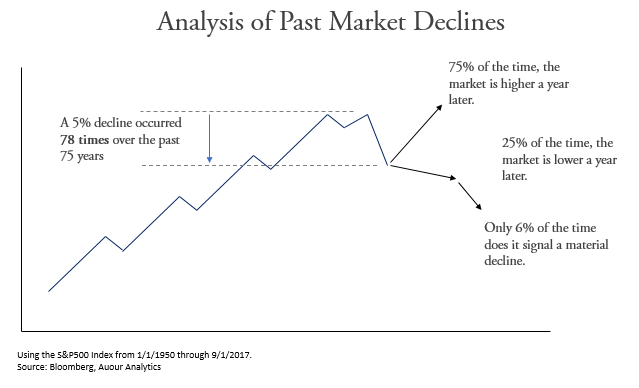

Rough periods in global markets are not abnormal. In our September 2017 newsletter, we discussed how short and shallow market corrections happen with regularity. We view the current environment in that same light. We don’t think this downturn will be among the 6 percent (see below) that signal a material decline.

Not all is smooth as a sow’s ear, though, which is why we have recently added to our cash position.

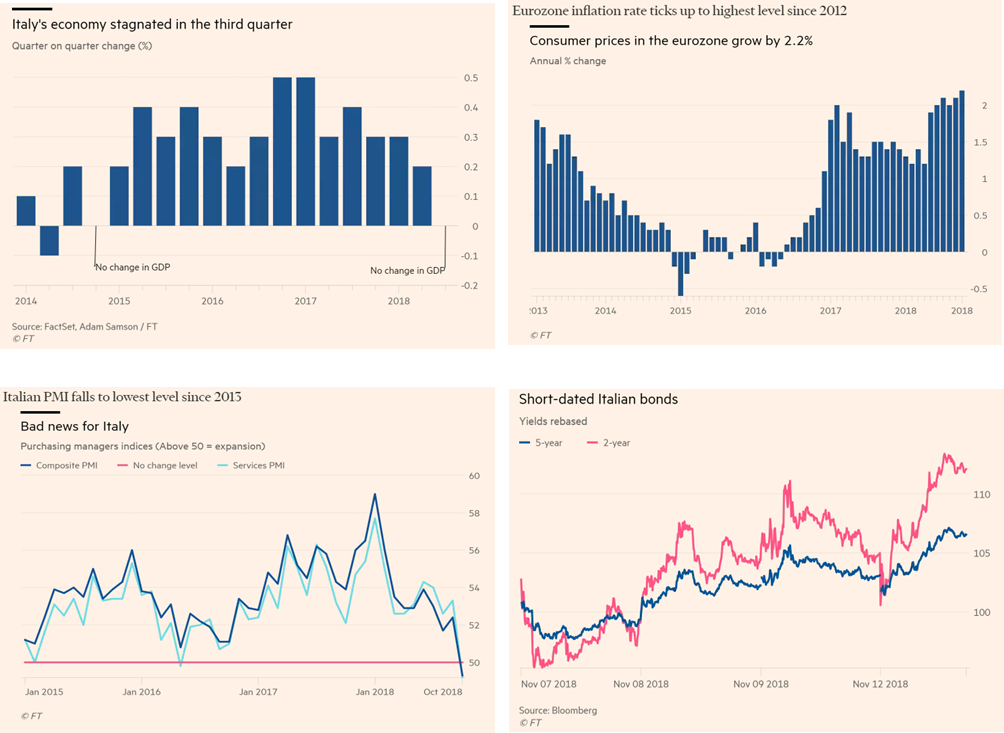

What are the rough patches? Those that have been feeding at the debt trough. The largest debtor in Europe, Italy, is experiencing a slow-motion crash. With rising inflation, a weakening economy, and a growing sense that no solution will be painless, the E.U. will need to buckle up and ride out the storm. Kicking the can down the road is no longer an option. Though not an imminent threat, like Greece was in 2010, 2012, and 2015, the charts below show that the investment markets are already building in the expectation that the Italian Job (a great movie) will not end well or quickly.

What are the rough patches? Those that have been feeding at the debt trough. The largest debtor in Europe, Italy, is experiencing a slow-motion crash. With rising inflation, a weakening economy, and a growing sense that no solution will be painless, the E.U. will need to buckle up and ride out the storm. Kicking the can down the road is no longer an option. Though not an imminent threat, like Greece was in 2010, 2012, and 2015, the charts below show that the investment markets are already building in the expectation that the Italian Job (a great movie) will not end well or quickly.

Throw into this a debt-heavy and weakening China corporate sector, the rapidly approaching Brexit, and Germany now getting the sniffles, and the global investor base is seeing little reason to hold firm in the face of uncertainty.

Our model indicates a more defensive position is appropriate, and we have raised cash levels accordingly*. Although it’s never fun to experience market corrections, they are a part of life and will erase themselves with time. Everyone has the 2008 meltdown in their minds. Our models are not suggesting such an event at this time. U.S. banks are well capitalized, and the consumer is healthy. We have a demographic surge in front of us that is a long-term phenomenon. It’s in the international markets that problems are expressing themselves and it might take time to recover. We have moved our already low exposure to the international market even lower, and we see times like these as preparation for a better entry point.

The historical benefit of investing in public equities does not come without some cost. And that cost is volatility and temporary moments of fear. We believe that our movements to cash have been proactive and will lead to a lower overall cost of investing. Patience is on our side as long as we do not act like hogs.

* Last Friday, we increased the tactical cash positions in all strategies as credit markets added to our increasing level of concern. Our equity strategies are now between 25-35% cash. Our balanced strategies have at least 20% cash and half its normal equity exposure or less, and our fixed income strategy is holding 20% cash and no high yield credit.